The functions developped in rjdmarkdown are:

-

print_preprocessing()for the pre-processing model;

-

print_decomposition()for the decomposition;

-

print_diagnostics()to print diagnostics tests on the quality of the seasonal adjustment.

The result is different between X-13ARIMA and TRAMO-SEATS models.

library(rjdmarkdown)

library(RJDemetra)

sa_x13 <- x13(ipi_c_eu[, "FR"])

sa_ts <- tramoseats(ipi_c_eu[, "FR"])X-13-ARIMA model

print_preprocessing(sa_x13)Pre-processing (RegArima)

Summary

372 observations

Trading days effect (7 variables)

Easter [1] detected

4 detected outliers

Likelihood statistics

Number of effective observations = 359

Number of estimated parameters = 17

Loglikelihood = -799.084, AICc = 1633.964, BICc = 1.855

Standard error of the regression (ML estimate) = 2.218

ARIMA model

| Coefficients | Std. Error | T-stat | P (> | t|) | ||

|---|---|---|---|---|---|

| Phi(1) | 0.000 | 0.108 | 0.003 | 0.998 | |

| Phi(2) | 0.169 | 0.074 | 2.278 | 0.023 |

|

| Theta(1) | -0.549 | 0.102 | -5.396 | 0.000 | *** |

| BTheta(1) | -0.666 | 0.042 | -15.775 | 0.000 | *** |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ’ ’ 1 | |||||

| ARIMA (2,1,1)(0,1,1) |

Regression model

| Coefficients | Std. Error | T-stat | P (> | t|) | ||

|---|---|---|---|---|---|

| Monday | 0.559 | 0.228 | 2.453 | 0.015 |

|

| Tuesday | 0.882 | 0.228 | 3.864 | 0.000 | *** |

| Wednesday | 1.040 | 0.229 | 4.535 | 0.000 | *** |

| Thursday | 0.049 | 0.229 | 0.215 | 0.830 | |

| Friday | 0.911 | 0.230 | 3.964 | 0.000 | *** |

| Saturday | -1.578 | 0.228 | -6.927 | 0.000 | *** |

| Leap year | 2.154 | 0.705 | 3.054 | 0.002 | ** |

| Easter [1] | -2.380 | 0.454 | -5.242 | 0.000 | *** |

| TC (4-2020) | -35.592 | 2.173 | -16.377 | 0.000 | *** |

| AO (3-2020) | -20.890 | 2.180 | -9.582 | 0.000 | *** |

| AO (5-2011) | 13.499 | 1.857 | 7.269 | 0.000 | *** |

| LS (11-2008) | -12.549 | 1.636 | -7.673 | 0.000 | *** |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ’ ’ 1 |

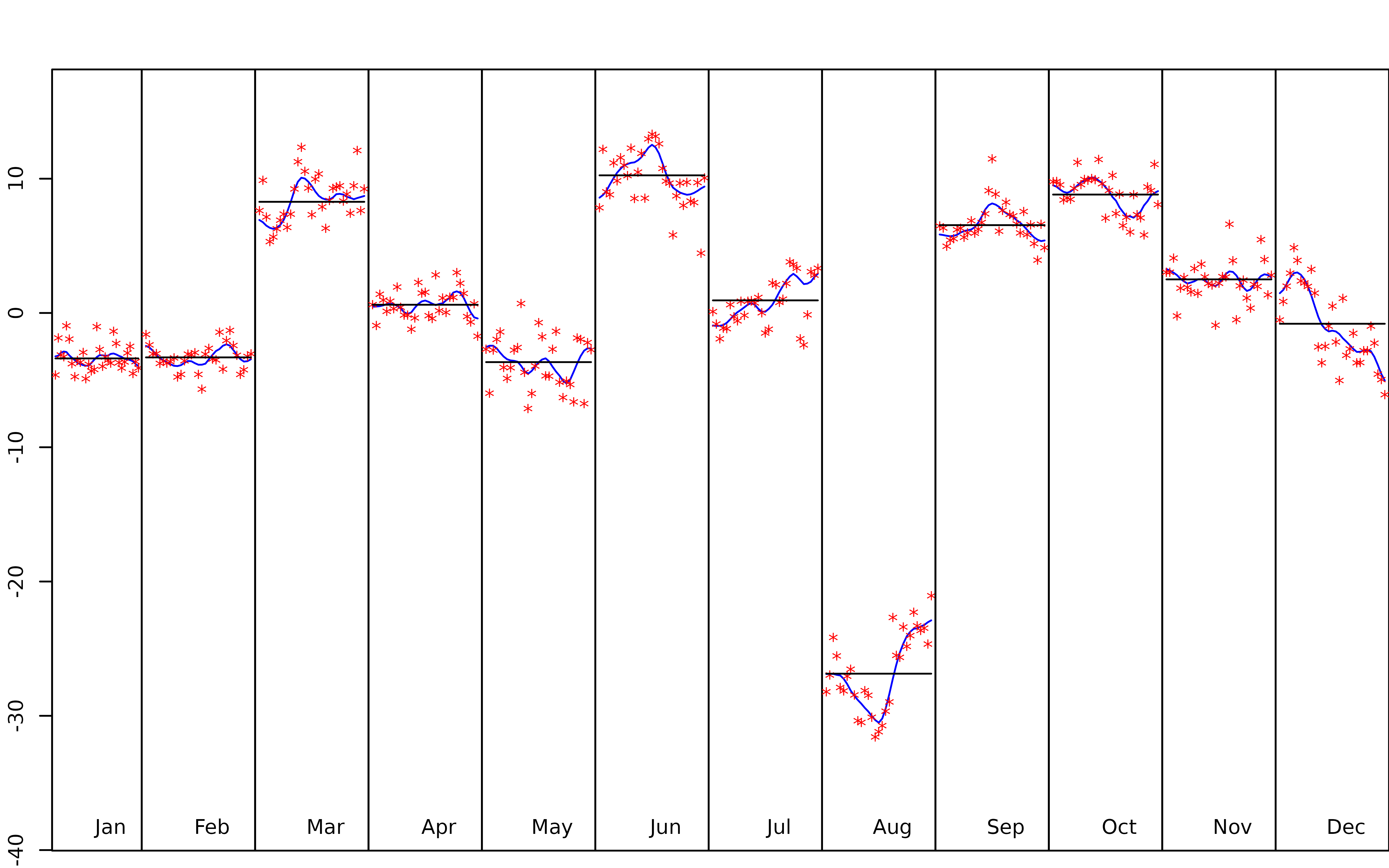

print_decomposition(sa_x13, caption = NULL)Decomposition (X-11)

Mode: additive

S-I Ratio

| Value | Description | |

|---|---|---|

| M-1 | 0.163 | The relative contribution of the irregular over three months span |

| M-2 | 0.089 | The relative contribution of the irregular component to the stationary portion of the variance |

| M-3 | 1.181 | The amount of period to period change in the irregular component as compared to the amount of period to period change in the trend |

| M-4 | 0.558 | The amount of autocorrelation in the irregular as described by the average duration of run |

| M-5 | 1.020 | The number of periods it takes the change in the trend to surpass the amount of change in the irregular |

| M-6 | 0.090 | The amount of year to year change in the irregular as compared to the amount of year to year change in the seasonal |

| M-7 | 0.083 | The amount of moving seasonality present relative to the amount of stable seasonality |

| M-8 | 0.244 | The size of the fluctuations in the seasonal component throughout the whole series |

| M-9 | 0.062 | The average linear movement in the seasonal component throughout the whole series |

| M-10 | 0.272 | The size of the fluctuations in the seasonal component in the recent years |

| M-11 | 0.256 | The average linear movement in the seasonal component in the recent years |

| Q | 0.368 | |

| Q-M2 | 0.402 | |

| Final filters: M3x5, Henderson-13 terms |

| Component | |

|---|---|

| Cycle | 2.251 |

| Seasonal | 59.750 |

| Irregular | 1.067 |

| TD & Hol. | 2.610 |

| Others | 33.718 |

| Total | 99.395 |

print_diagnostics(sa_x13)| P (> | t|) | ||

|---|---|---|

| mean | 0.899 | |

| skewness | 0.880 | |

| kurtosis | 0.034 |

|

| ljung box | 0.000 | *** |

| ljung box (residuals at seasonal lags) | 0.212 | |

| ljung box (squared residuals) | 0.024 |

|

| qs test on sa | 0.985 | |

| qs test on i | 0.865 | |

| f-test on sa (seasonal dummies) | 0.958 | |

| f-test on i (seasonal dummies) | 0.893 | |

| Residual seasonality (entire series) | 0.876 | |

| Residual seasonality (last 3 years) | 0.906 | |

| f-test on sa (td) | 0.987 | |

| f-test on i (td) | 0.993 | |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ’ ’ 1 |

TRAMO-SEATS model

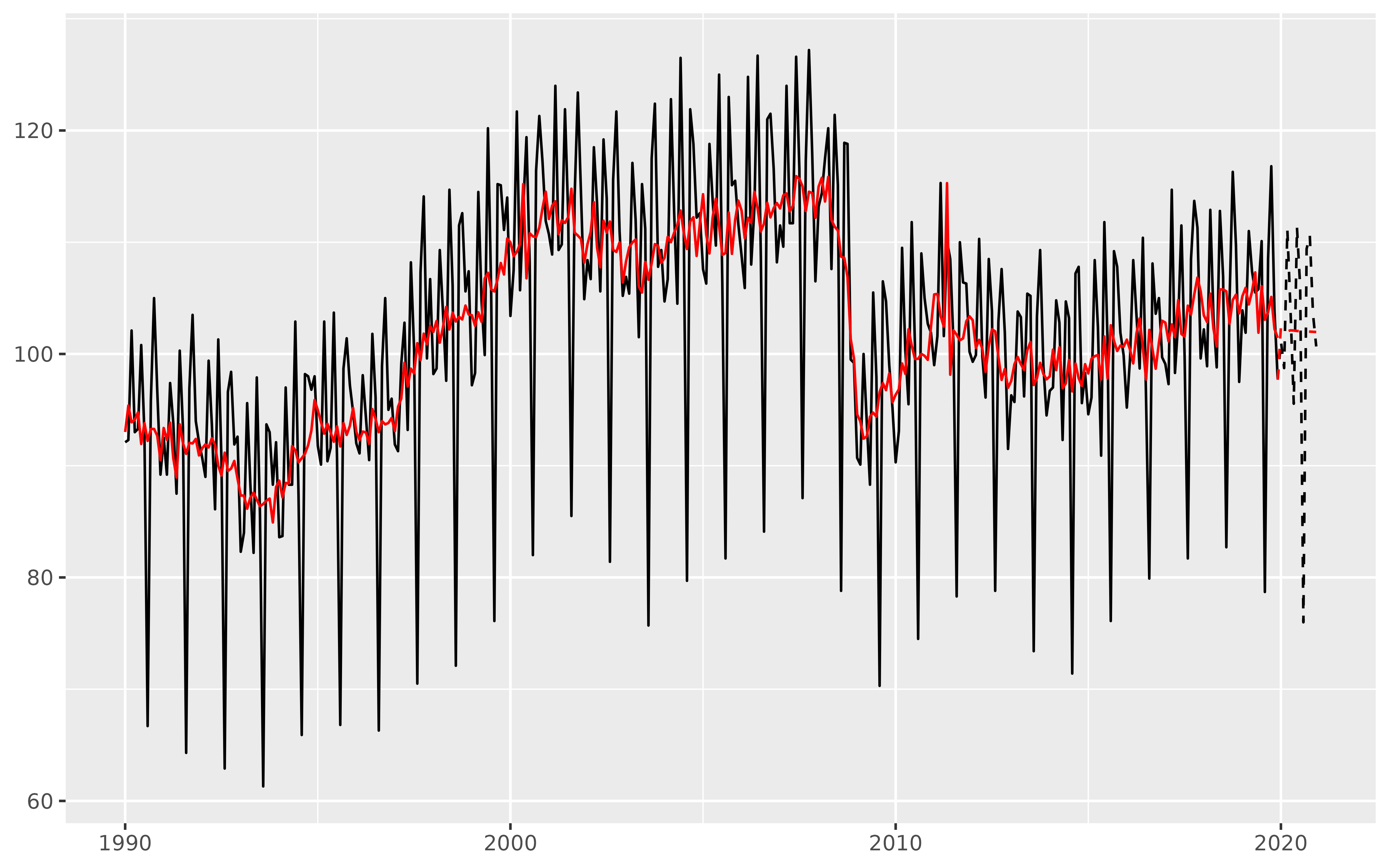

Some others graphics can also be added with the ggdemetra

package, for example to add the seasonally adjusted series and its

forecasts:

library(ggdemetra)

ggplot(data = ipi_c_eu_df, mapping = aes(x = date, y = FR)) +

geom_line() +

labs(title = NULL,

x = NULL, y = NULL) +

geom_sa(component = "y_f", linetype = 2,

frequency = 12, method = "tramoseats") +

geom_sa(component = "sa", color = "red") +

geom_sa(component = "sa_f", color = "red", linetype = 2)

Seasonal adjustment of the French industrial production index

print_preprocessing(sa_ts)Pre-processing (Tramo)

Summary

372 observations

Trading days effect (2 variables)

Easter [6] detected

4 detected outliers

Likelihood statistics

Number of effective observations = 359

Number of estimated parameters = 11

Loglikelihood = -816.075, AICc = 1654.912, BICc = 1.852

Standard error of the regression (ML estimate) = 2.326

ARIMA model

| Coefficients | Std. Error | T-stat | P (> | t|) | ||

|---|---|---|---|---|---|

| Phi(1) | 0.403 | 0.051 | 7.845 | 0.000 | *** |

| Phi(2) | 0.288 | 0.051 | 5.616 | 0.000 | *** |

| BTheta(1) | -0.664 | 0.042 | -15.865 | 0.000 | *** |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ’ ’ 1 | |||||

| ARIMA (2,1,0)(0,1,1) |

Regression model

| Coefficients | Std. Error | T-stat | P (> | t|) | ||

|---|---|---|---|---|---|

| Week days | 0.699 | 0.032 | 22.016 | 0.000 | *** |

| Leap year | 2.323 | 0.690 | 3.367 | 0.001 | *** |

| Easter [6] | -2.515 | 0.436 | -5.773 | 0.000 | *** |

| AO (5-2011) | 13.468 | 1.787 | 7.535 | 0.000 | *** |

| TC (4-2020) | -22.213 | 2.205 | -10.072 | 0.000 | *** |

| TC (3-2020) | -21.039 | 2.217 | -9.492 | 0.000 | *** |

| AO (5-2000) | 6.739 | 1.794 | 3.757 | 0.000 | *** |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ’ ’ 1 |

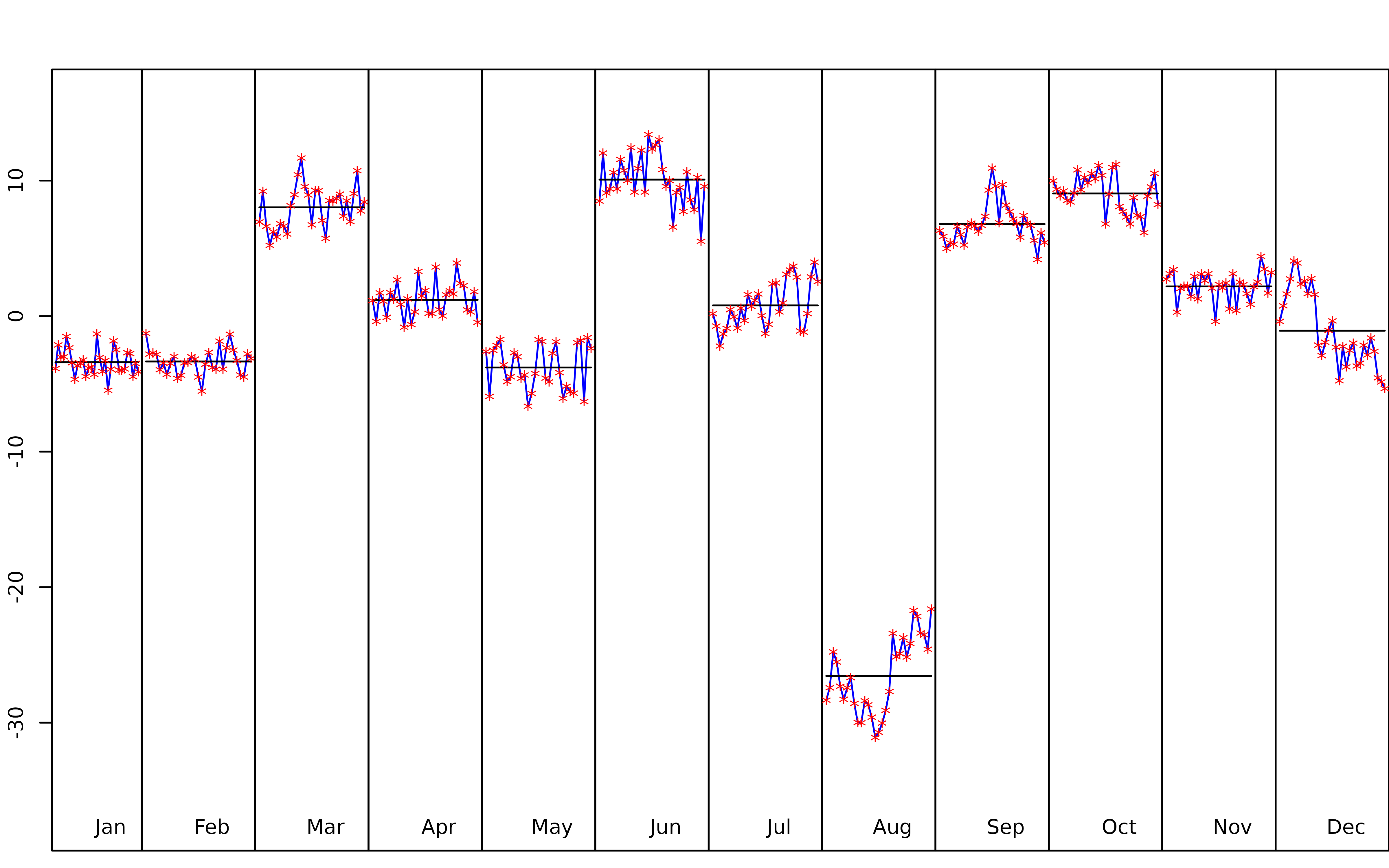

print_decomposition(sa_ts, caption = NULL)Decomposition (SEATS)

Mode: additive

S-I Ratio

Model

AR:

D:

MA:

SA

AR:

D:

MA:

Innovation variance: 0.704

Trend

D:

MA:

Innovation variance: 0.061

Seasonal

D:

MA:

Innovation variance: 0.043

Transitory

AR:

MA:

Innovation variance: 0.053

Irregular

Innovation variance: 0.203

| Component | |

|---|---|

| Cycle | 6.087 |

| Seasonal | 80.528 |

| Irregular | 0.965 |

| TD & Hol. | 3.590 |

| Others | 8.102 |

| Total | 99.271 |

print_diagnostics(sa_ts)| P (> | t|) | ||

|---|---|---|

| mean | 0.988 | |

| skewness | 0.413 | |

| kurtosis | 0.095 | . |

| ljung box | 0.010 | ** |

| ljung box (residuals at seasonal lags) | 0.192 | |

| ljung box (squared residuals) | 0.000 | *** |

| qs test on sa | 1.000 | |

| qs test on i | 1.000 | |

| f-test on sa (seasonal dummies) | 1.000 | |

| f-test on i (seasonal dummies) | 1.000 | |

| Residual seasonality (entire series) | 1.000 | |

| Residual seasonality (last 3 years) | 0.974 | |

| f-test on sa (td) | 0.152 | |

| f-test on i (td) | 0.224 | |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ’ ’ 1 |

Directly create a R Markdown file

A R Markdown can also directly be created and render with the

create_rmd function. It can take as argument a

SA, jSA, sa_item,

multiprocessing (all the models of the

multiprocessing are printed) or workspace object (all the

models of all the multiprocessing of the

workspace are printed).

The print of the pre-processing, decomposition and diagnostics can

also be customized with preprocessing_fun,

decomposition_fun and diagnostics_fun

arguments. For example, to reproduce the example of the previous

section:

preprocessing_customized <- function(x){

library(ggdemetra)

y <- get_ts(x)

data_plot <- data.frame(date = time(y), y = y)

p <- ggplot(data = data_plot, mapping = aes(x = date, y = y)) +

geom_line() +

labs(title = NULL,

x = NULL, y = NULL) +

geom_sa(component = "y_f", linetype = 2,

frequency = 12, method = "tramoseats") +

geom_sa(component = "sa", color = "red") +

geom_sa(component = "sa_f", color = "red", linetype = 2)

plot(p)

cat("\n\n")

print_preprocessing(sa_ts)

}

decomposition_customized <- function(x){

print_decomposition(x, caption = NULL)

}

output_file <- tempfile(fileext = ".Rmd")

create_rmd(sa_ts, output_file, output_format = "html_document",

preprocessing_fun = preprocessing_customized,

decomposition_fun = decomposition_customized,

knitr_chunk_opts = list(

fig.pos = "h", results = "asis",

fig.cap =c("Seasonal adjustment of the French industrial production index",

"S-I Ratio"),

warning = FALSE, message = FALSE, echo = FALSE)

)

# To open the file:

browseURL(sub(".Rmd",".html", output_file, fixed= TRUE))Several models can also be printed creating a workspace:

wk <- new_workspace()

new_multiprocessing(wk, "sa1")

add_sa_item(wk, "sa1", sa_x13, "X13")

add_sa_item(wk, "sa1", sa_ts, "TramoSeats")

# It's important to compute the workspace to be able to import the models

compute(wk)

output_file <- tempfile(fileext = ".Rmd")

create_rmd(wk, output_file, output_format = "html_document",

output_options = list(toc = TRUE,

number_sections = TRUE))

# To open the file:

browseURL(sub(".Rmd",".html", output_file, fixed= TRUE))Reproductibility

To produce this document, the knitr options were set as

followed:

knitr::opts_chunk$set(

collapse = TRUE,

comment = "#>", out.width = "100%",

fig.dim = c(7, 5),

warning = FALSE, message = FALSE

)And the options results='asis', fig.cap = "S-I Ratio"

were used in the chunks.